Does the US Intentionally "Want" a Recession?

President Trump's statement that he "does not focus on the market" seems profound.

Original Author: The Kobeissi Letter

Original Translation: Deep Tide TechFlow

Is the U.S. Government Expecting an Economic Recession?

By 2025, the U.S. will have $92 trillion in debt maturing or needing to be refinanced. Faced with this massive refinancing, the quickest way to lower rates may be to induce an economic recession.

But can the U.S. benefit from a market crash?

Over the past two months, the 10-year treasury yield has dropped by around 60 basis points. This is partly due to market expectations of cuts to the government's discretionary sector spending. However, it is also tied to increased uncertainty and the rising possibility of a U.S. economic recession.

An economic recession almost guarantees a rate cut.

But why does an economic recession signify a rate cut?

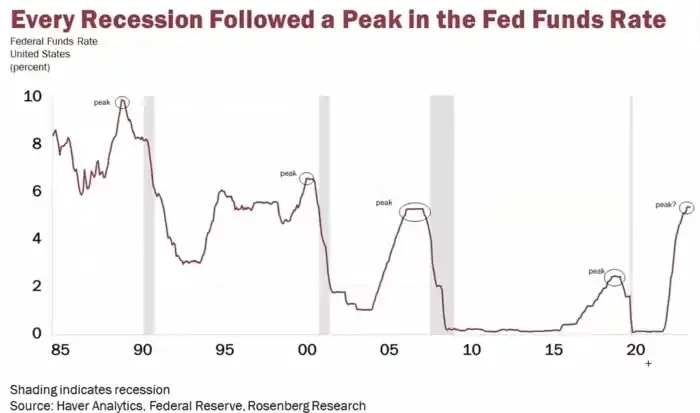

Since the 1980s, every U.S. economic recession has occurred after the federal funds rate has peaked. When economic growth stalls, the Fed acts to "stimulate" the economy. This means lowering rates to reduce the cost of capital and encourage spending.

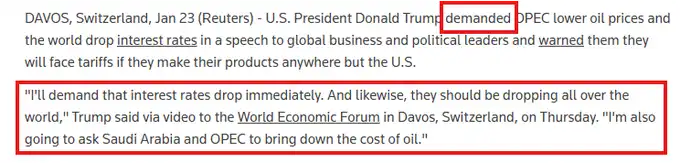

Since the start of the trade war, U.S. economic growth expectations have plummeted significantly. Meanwhile, oil prices have hit a new 6-month low. Interestingly, President Trump has repeatedly expressed his desire to lower oil prices to alleviate inflationary pressures.

On January 25, President Trump claimed he has a solution to the Fed's more than 3-year fight against inflation. He called on the Organization of the Petroleum Exporting Countries (OPEC) to lower oil prices and urged a global rate cut.

However, the quickest way to lower oil prices is most likely through a demand-reducing economic recession.

In a recent interview with Fox News, President Trump mentioned that he would prioritize lowering rates.

He said, "Rates are coming down... and I hope they do because I love the country and I'd like to see the country thrive." This quote is from @amitisinvesting's report.

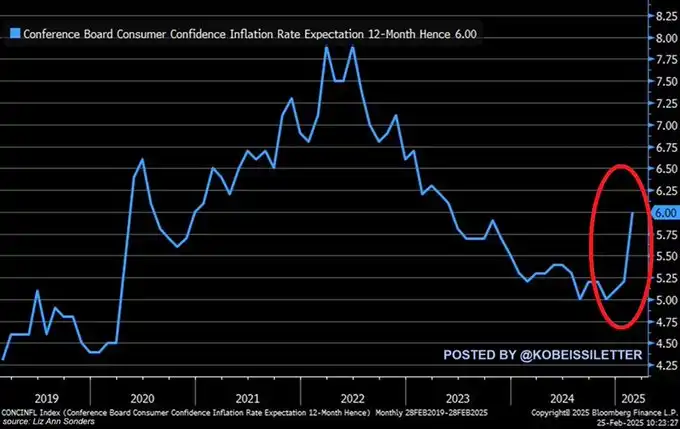

Next, let's take a look at the inflation data.

American consumers believe that the inflation rate for the next 12 months will rise to +6.0%, the highest level since May 2023. This marks the third consecutive month of rising inflation expectations.

Inflation is on the rise, rate cuts are postponed, yet interest rates are declining.

The market is pricing in an economic recession.

In the escalating trade war of soaring inflation, a sharp rate cut is almost inevitably a precursor to an economic recession. Furthermore, on March 6, President Trump stated that he doesn't even pay attention to the stock market. The reality, however, is that, just as we saw in his first term, Trump has always been watching the market.

President Trump's statement of "not paying attention to the market" is significant.

In a scenario where he clearly does pay attention to the market, this is actually a signal he is sending to Wall Street, indicating his willingness to lower interest rates and reduce the trade deficit at all costs, even if it means potentially triggering an economic recession.

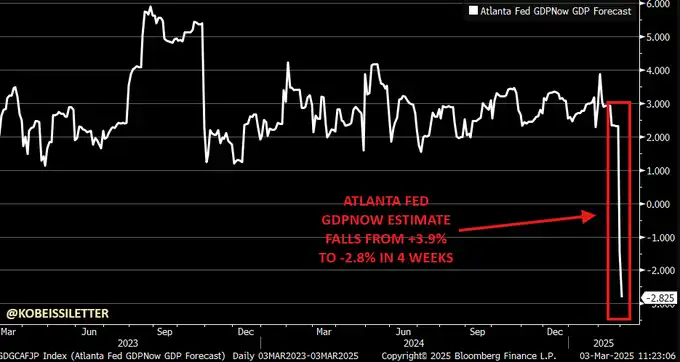

In the chaos of the trade war, we see a significant downward revision in economic growth expectations. The Atlanta Fed last week lowered its GDP growth forecast for the first quarter of 2025 to as low as -2.8%. Therefore, we see a sharp increase in market expectations for rate cuts last week.

Is this intentional?

High-interest rates are the biggest challenge facing the U.S. government.

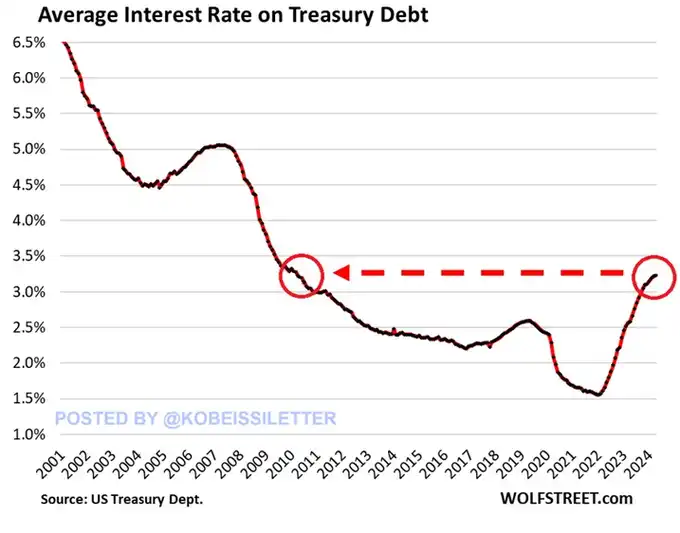

As interest rates soar, the cost of debt interest payments increases significantly. Currently, the average interest rate on the U.S.'s $36.2 trillion national debt is 3.2%, hitting the highest level since 2010. The U.S. government needs a rate cut more than anyone.

Furthermore, a rate cut is imminent:

The U.S.'s $9.2 trillion debt maturity is heavily concentrated in the first half of 2025, with 70% of the debt needing refinancing from January to June 2025.

The average interest rate on this debt is expected to rise by about 1 percentage point.

Moreover, efforts to reduce deficit spending in the U.S. will not happen overnight.

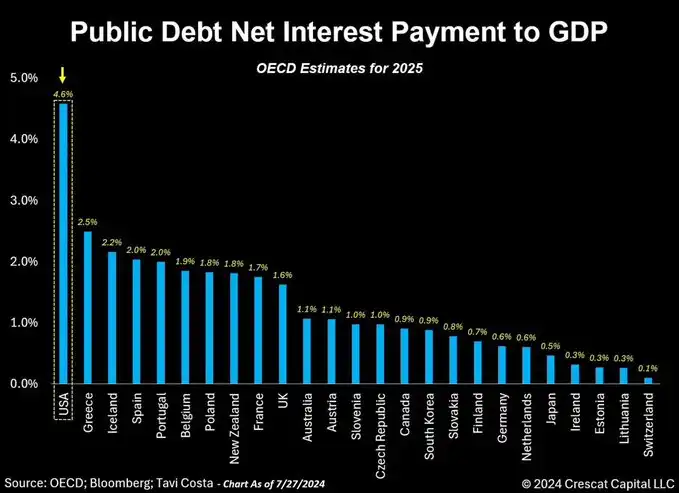

In the 2024 fiscal year, the United States had expenditures of up to $7.8 trillion, while income was only about $5.0 trillion. This means that for every $1 of income generated, there was $1.56 in costs. The shadow of a debt crisis will loom over the United States for a long time to come.

These significant changes in the macroeconomic landscape will have a broad impact on the entire market, and we are currently and will continue to seize opportunities from them.

Interested in how we trade the market? Click the link below to subscribe to our premium analysis and alert service: https://www.thekobeissiletter.com/pricing

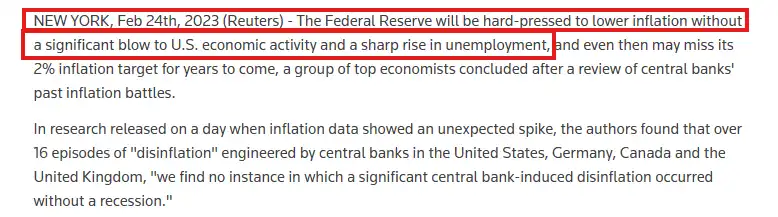

Finally, let's go back to 2023 when the Federal Reserve was on the verge of calling for an economic recession to curb inflation.

In February 2023, many studies indicated that an economic recession might be the only solution. Subsequently, the Fed shifted to the narrative of a "soft landing," but this strategy has so far failed to lower interest rates.

The reality is that the U.S. debt crisis is currently the most severe yet most neglected crisis. While President Trump has acknowledged this, it may be too late. An economic recession may be the only solution to lower interest rates.

Follow us @KobeissiLetter for real-time analysis updates.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

An FTX/Alameda-associated address released 185,000 SOL stakes

Ethereum's Ether (ETH) Drops Below $2,000, Onchain Data Suggests Further Decline

Modular blockchain network Hemi mainnet launched